If you read the UK education press at all, you’ll have noticed a serious uptick recently in the number of stories describing the current student loan system as “a scam” by Government back-bench MPs and “a mess” by a former Deputy PM who played a large role in designing it. What’s going on, you ask? How bad is it? Well..

The problem with student finance in the UK is that Tony Blair and Gordon Brown, in their haste to modernize the British economy and expand higher education funding in the early 2000s, based their policy on two things. 1) It shouldn’t cost the treasury too much and 2) it definitely shouldn’t cost parents a single cent. This left only one option: higher tuition fees, but paid not by students at the point of service delivery, but rather by graduates, decades down the road.

Thus, in 2006, the UK moved to a system where universities could charge up to £3000/year, and students would have guaranteed access to a loan to cover this amount. They could also receive loans as well as grants for what the Brits call “maintenance” (i.e. living costs). Both loans were repayable on an income-contingent basis, where the threshold for repayment was £15,000 and payment above that level was 9%. So, if your income was £30,000, then your payment would be (£30,000-£15,000)*.09 = £1350. These loans would be repayable for a period of 25 years, after which any outstanding balance would be forgiven. The value of the loans was linked to inflation, but the loans carried no real interest.

Two asides to make here right now. First, maintenance loans were usually larger than tuition loans. And this was a problem because UK students have a much higher rate of studying away from home than any other group of students in the world. Living with your parents is very much the minority option for 18-21 year-olds, which, you know, is kind of expensive. Second: raising repayment thresholds reduces the amount students have to pay into the system and increases the amount governments end up having to pay at the end of the repayment period; reducing them achieves the reverse. Pay attention to this because it ends up having a big effect on policy over time.

There were no big policy changes for the next six years, including no change to the repayment threshold. With inflation and economic growth, salaries rose and students were repaying more of their loans faster (and, conversely, the government was not having to pay as much money at the back end). But then, in 2012, the system changed again. Tuition was allowed to rise to a maximum of £9000, on the utterly misguided assumption that this would create price competition (it did not occur to Whitehall officials that in education markets, prices are – for better or worse – a signal of quality, and literally no one wants to play the role of Walmart). And this was combined with a massive public disinvestment from direct support of universities. The 2006 deal was that students would pay “extra” in order to expand and improve the system; the 2012 deal was that students had to pay 3x because the government didn’t feel like paying for universities anymore. And while loans were available to cover the difference, these loans now carried interest at a rate of inflation plus 3% while in-study or if income was over 41,000 (if income in repayment was less than 41,000, interest remained equal to inflation, and yes, this was, and is, unnecessarily complicated). The mandatory repayment period was extended from 25 to 30 years. Oh, and the government began charging interest on the loan at a rate of inflation plus 3.1%.

Now, there was one piece of countervailing policy, and that was that loan thresholds were unfrozen and raised to £21,000, because with all the bad news government felt it needed to throw recent graduates a bone. But this created a problem. Debt and interest payments were being vastly increased, but at the same time, the rise in the threshold meant that students would pay less of it back over time. The early data indicated that roughly half of all sums lent would not, in the end, be repaid. So even though government was reducing its payments to universities in the short term, it was vastly increasing the amount of expected loan repayment in the long term.

The next big change was 2016/17, when the Conservative government decided to get rid of student grants entirely. Maintenance was now entirely delivered via loan. Debt levels went up accordingly. In 2018, the threshold was suddenly raised to £25,000 and indexed (good for students, bad for government), but then just as re-frozen again in 2022 at £27,295, re-unfrozen in 2025, and then re-re-frozen until 2030 at £29,385 (policy stability is not really a Whitehall strength).

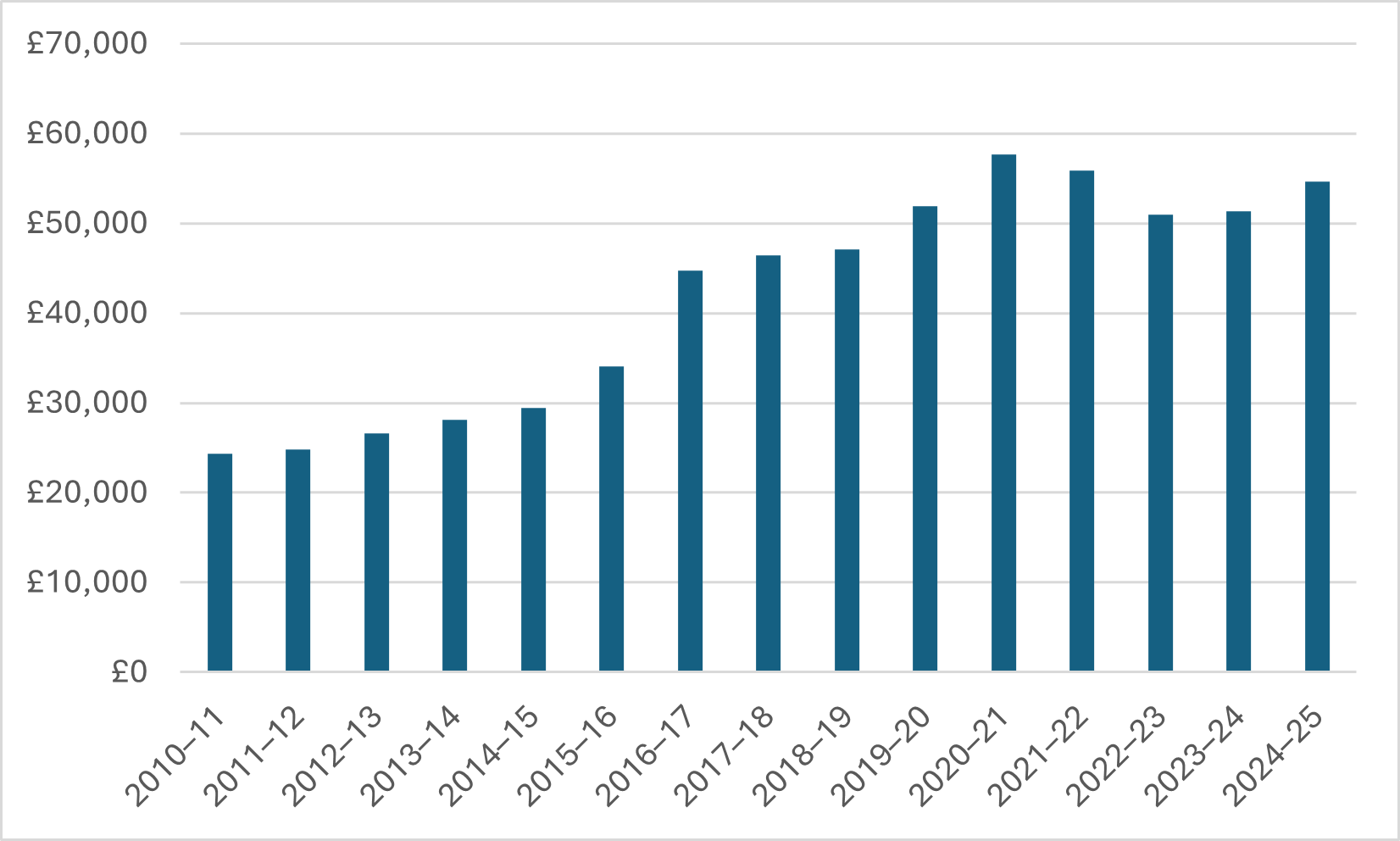

So, what has all this accomplished? Well, let’s start with debt levels. Figure 1 shows average student debt levels by graduating cohort, in constant 2025 GBP. In 2024-25, the average debt at graduation was over £50,000, or C$97,000 at current rates of exchange.

Figure 1: Student Loan Debt at Graduation by Graduating Cohort, England, 2010-11 to 2024-25

Now, when debts get this large, and you have positive interest rates, it’s easy to end up with what’s known as “negative amortization” – that is, your debt grows even if you aren’t adding to the borrowing. For students in the UK, this happens during studies because of the way interest is charged to students while they are in-study (to my knowledge, the UK is the only country other than Japan – where interest rates are barely positive to begin with – that does this). This can also happen if students are below the repayment threshold. According to tax data, on average spend about three years in the labour force before crossing the income threshold. On the one hand, that’s good for students in the short term: no repayment for three years. On the other hand, for students with average incomes, that means six years of interest accumulating before you make a single payment. For graduates with average levels of debt in 2024/25, that means adding another £11,000 (C$20,000) in debt before a student is able to start repayment.

Let me play this out a bit. In the example above, the graduate starts year 4 after graduation with a shade over £60,000 ($C110,000) in debt. At current levels of inflation/interest, that sum will grow by roughly £4,000 during year 4. In order for a student to pay that amount, they would need to be earning about £75,000 (C$137,250) just in order to cover interest and stop the debt from increasing. The median salary for all university graduates in the UK is just £42,000, meaning at current rates of inflation, the vast majority of students won’t just not pay back their loans, they will never even see their loans decrease in size.

There is no other student loan system in the world that is this badly designed. None even come close.

It’s not that most of these policies are indefensible on their own. Large debts with generous forgiveness? Makes sense. Income-contingent repayment? Works well in many countries. Interest on student loans? Not crazy: money has time-value, after all. But it’s the mix of policies which is both unworkable and utterly indefensible. And the root problem is that starting levels of debt are simply too high.

In my experience of working with international student loan systems, a reasonable rule of thumb is that student loan systems where students are actually charged interest more or less work up until the point where debt is equal to a year’s salary for a graduate and stop working after that. By this rule, student debt in the UK needs to come down by at least 50%. That requires reinstituting maintenance grants and it means going back to something like the status quo ante on tuition fees and funding for universities (it probably also means lowering the loan repayment threshold, but that’s a secondary issue)

Don’t expect this change to happen any time soon, though. Being penny-wise and pound-foolish is a deeply-held value at Treasury; the idea that they might need to spend more to rescue a system that is dangerous and workable simply doesn’t scan. So, for the foreseeable future, English students and graduates will continue to struggle with the worst student loan system in the world.

One Response

Perfect summary

Also not a progressive issue as well off parents can repay and charge their kids a lower rate if commercial interest !

You can’t even pay down a lump sum because repayment is still 9% of any salary above the threshold.

You didn’t mention selling the debt to a private “student loan company” because the EU wouldn’t allow the original offer balance sheet dodge (very Gordon Brown).