I’ve spent a lot of time recently talking about Ontario colleges, about how they have responded to persistent underfunding by via the international student business (either on their own or via public-private partnerships). But I have not spent so much time discussing the province’s other sector, the one which faced similar losses in government-controlled revenue but did not did not pursue international quit so arduously. So today, let’s talk about Ontario universities.

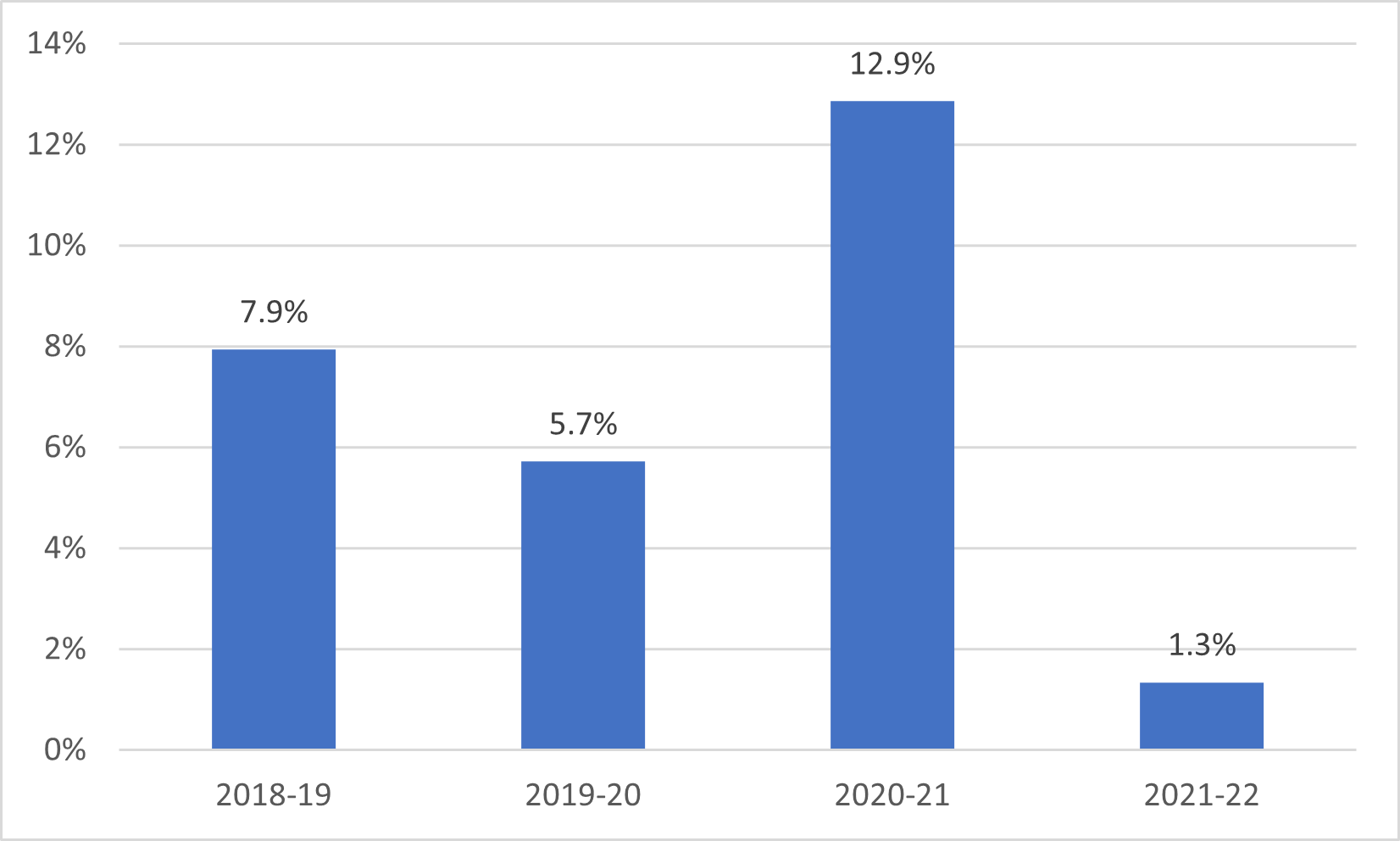

We can start by looking at financial data from the annual Financial Information of Universities and Colleges (FIUC) survey for the most recent 4 years. In Figure 1, I show the combined net income of Ontario universities from 2018-19 until 2021-22, the last year for which data is available. Although the 2018-19 year was technically the first year of the Ford government, in financial terms it was like last year of the Wynne government because none of the Ford government’s interventions – most notably the 10% reduction in tuition fees – kicked in until the following year. So, we can think of 2018-19 as kind of a “base” year. I have removed endowment income from the totals because the wild swings of the stock market, particularly around the 2020 fiscal year end, tend to exaggerate what happened.

Figure 1: Combined Net Income of Ontario Universities, Excluding Endowment Income, 2018-19 to 2021-22

Now, I should note that these numbers are not the numbers the institutions themselves normally use. The accounting definitions and conventions for the FIUC survey do not necessarily like up with what is in institutions’ own financial reports. Laurier looks less solid in its own accounts and TMU looks better. I don’t think this is a case of anyone cooking the books, it’s just that different types of reporting generate different results. So, the spread around the 1.3% average probably is not as big as figure 2 implies, but it is still probably significant.

So, the key question: what’s been going on since the end of fiscal ‘22? To answer this question, I looked for all institutions’ financial statements for 22-23 (Only about half of which are published yet) and any budget documents that are public for 22-23 or 23-24 (many institutions do not publish these). And let me tell you, what I see is a bit worrying.

First, there are a bunch of large universities – Guelph, McMaster, Ottawa, and Queen’s – that all seem to have lost something in the region of $20-40 million last year and plan to run significant deficits this year. Western ran a deficit about that large last year, (in part due to a decision to put $25 million in an Academic Renewal Endowment fund to support faculty Hiring for Equity-Deserving Groups) but is budgeting for a more-or-less break-even budget this year. TMU, which in its own books posted about a 1.5% surplus in 2021-22 rather than the 10% deficit it showed to Statscan, saw a $31-million drop in its fiscal position in 22-23, and was budgeting for zero in 23-24, albeit with an across-the-board 3.5% budget cut. Carleton, which used to run $100 million surpluses, now looks to be running small deficits.

Waterloo, Laurier, OCAD, UOIT, Trent, Windsor, Brock, Lakehead, and Nipissing all seem to be budgeting for either zero or small deficits. Again, we need to be careful here because a) budgets are political documents and b) university budgets usually only cover operations and it could well be that all the surpluses are happening in other areas. They might be higher or lower than this.

There are two institutions where post-2021-22 financial futures seem absolutely fine. The first is the University of Toronto (big surprise). In 2022-23, Toronto increased its overall surplus by $100 million over 2021-22. Their budget for 23-24 is formally “balanced”, but I’d lay money it will do at least as well this year as last. And then there is Algoma, whose financial strategy resembles some Northern Ontario colleges, except that it is running its own effectively-primarily-Indian satellite campus in Brampton rather than contracting out to a private entity. Algoma has not published any information on finances or budget since the end of the 21-22 fiscal but given that it is aiming to double the size of its GTA campus, my guess is that it, like U of T, will probably be significantly better off in 2023-24 than it was in 2021-22.

In short, what you have are two institutions likely to be in the 5% safety zone this year. Most are below it, and a few of the big ones are in outright deficit not just last year, not just this year, but for the foreseeable future. The province’s universities – unlike the colleges – are in the middle of a very rough ride indeed. And because unlike the colleges, they chose not to dive headfirst into the international student market.

This isn’t a disaster, though. A disaster is something that is unforeseen and unpredictable. This, rather, is a deliberate crisis which has been decades in the making, the result of a pan-partisan commitment to public underfunding of universities, and a Ford-era cut/freeze to domestic tuition fees. It only ends when universities start collapsing or when the Ontario government wakes up from the delusion that it can have a world-class system of higher education while investing less than half of what the other nine provinces do.