Governments always face a choice between access and excellence: does it make more sense to focus resources on a few institutions in order to make them more “world-class”, or does it make sense to build capacity more widely and increase access? During hard times, these choices become more acute. In the US, for instance, the 1970s were a time when persistent federal budget deficits as a result of the Vietnam War, combined with a period of slow growth, caused higher education budgets to contract. Institutions often had to choose between their access function and their research function, and the latter did not always win.

My question today (excerpted from the paper I gave in Shanghai on Monday) is: how are major OECD countries handling that same question in the post-2008 landscape?

Below, I have assembled data on real institutional expenditures per-student in higher education, in ten countries: Canada, the US, the UK, Australia, Sweden, Switzerland, France, Germany, the Netherlands, and Japan. I use expenditures rather than income because the latter tends to be less consistent, and is prone to sudden swings. Insofar as is possible, and in order to reduce the potential impact of different reporting methods and definitions of classes of expenditure, I use the most encompassing definition of expenditures given the available data. The availability of data across countries is uneven; I’ll spare you the details, but it’s reasonably good in the US, the UK, Canada, Australia, and Sweden, decent in Switzerland, below-par in Japan, the Netherlands, and Germany, and godawful in France. For the first six countries, I can compare with reasonable confidence how “top” universities (as per yesterday, I’m defining “top” as being among the top-100 of the Academic Ranking of World Class Universities, or the ARWU-100 for short). In the six countries with the best data, I can differentiate between ARWU-100 universities and the rest; in the other four, I have only partial data, which nevertheless leads me to believe that the results for “top” universities is not substantially different from what happened to all institutions.

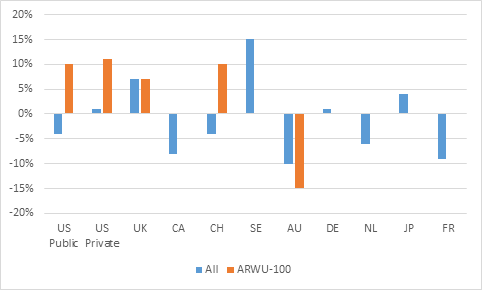

Figure 1 basically summarizes the findings:

Figure 1: Changes in Real Per-Student Funding Since 2008 for ARWU-100 and All Universities, Selected OECD Countries

Here’s what you can take from that figure:

1) Since 2008, total per-student expenditures have risen in only three countries: the UK, Sweden, and Japan. In the UK, the increase comes from the massive new tuition fees introduced in 2012. In Sweden, a lot of the per-student growth comes from the fact that enrolments are decreasing rapidly (more on that in a future blog). In Germany, per-student expenditure is down since 2008, but way up since 2007. The reason? The federal-länder “higher education pact” raised institutional incomes enormously in 2008, but growth in student numbers (a desired outcome of the pact) meant that this increase was gradually whittled away.

2) “Top” Institutions do better than the rest of the university sector in the US, Canada, and Switzerland (but for different reasons), but worse in Sweden and Australia. Some of this has to do with differences in income patterns, but an awful lot has to do with changes in enrolment patterns too, which are going in different directions in different countries.

3) Australian universities are getting hammered. Seriously. Since 2008, their top four universities have seen their per-student income fall by 15% in real terms. A small portion of that seems to be an issue of some odd accounting that elevated expenditures in 2008, and hence exaggerates expenses in the base year; but even without that, it’s a big drop. You can see why they want higher fees.

4) Big swings in funding don’t make much short-term difference in rankings – at least at the top. Since 2008, top-100 universities in the US have increased their per-student expenditure by 10%, while Australian unis have fallen by 15%. That’s a 25% swing in total. And yet there has been almost no relative movement between the two in any major rankings. When we think about great universities, we need to think more about stocks of assets like professors and laboratories, and less about flows of funds.

So there’s no single story around the world, but there are some interesting national policy choices out there.

If anyone’s interested in the paper, I will probably post it sometime next week after I fix up a couple of graphs: if you can’t wait, just email me (ausher@higheredstrategy.com), and I’ll send you a draft.

Tweet this post

Tweet this post